There is no possible place to start with Kevin's dog and pony show here. There is far too much to debunk, and the ease of doing so is too light to make it really much of a challenge.

I can pick any one of the pellets Graham has shot from his scattergun in this thread and easily and surgically dismantle it, but spending an entire day arguing with a juvenile version of Chris Matthews is not my cup of tea. I have far better things to do.

The really important thing here is to demonstrate, through a little logical argument and the pointing out of some simple, basic facts, the degree to which Graham carefully and at only a surface level, cherry picks the data and claims he uses while ignoring salient variables and complexities that would monkey wrench his arguments.

Let's take his claims about the Bush tax cuts, just for one example.

In the first place, the

Wall Street Journal is not a "right wing" paper; only its editorial section is conservative. But this is only the beginning of a plethora of errors and mistakes Graham makes because he's really not interested in understanding what he's talking about, just winning an internet debate with a "right winger".

Firstly, the total new jobs created between the Budget Reconciliation Act of 1993 and the end of Clinton's term was actually 21.4 million, not 23 million. Secondly, as there is no reason to believe, historically or as a matter of substantive economic theory, that increases in tax rates create greater economic activity (indeed, this is counter-intuitive on its face), other factors present during the Clinton years must come into play as causal factors in the growing economy at that time, including the 1997 tax cuts, which most certainly stimulated the economy and perhaps softened the negative effects of Clinton's substantial tax increases, negating economic weakness that did not materialize because of the stimulative effects of those tax deceases.

Thirdly, Welfare reform, lower government spending as a share of gross domestic product, the highly successful NAFTA, and other variables combined with the stimulative effect of lowering

taxes on productive economic activity were probably the main wellsprings of the healthy economy in Clinton's second term, not tax hikes, which decease productive economic activity, discourage investment and job creation, and shrink the total tax base.

Did the Bush tax cuts decrease revenue? Certainly:

But notice, this was only during the period in which the tax cuts were being phased in. Revenues fall until 2003, and then take off again dramatically. What do graphs like this, of which Kevin is so fond and which he tends to use in lieu of critical argument, actually show us?

Not much beyond correlation, which is why one must have a broad understanding of a number of variables involved in any such analysis as well as a substantive theoretical background from which to interpret statistical graphs such as this, which are after all, human methodological constructions that only capture a limited and compartmentalized snapshot of much more complex phenomena.

Did the Bush tax hikes decease or raise revenue? Well, what a graph like this one tells us is that revenues deceased as the tax cuts were phased in, and then took of after full implementation. But is this lag in revenue increase fully a product of the tax cuts? Kevin ignores confounding variables such as the major recession under way between 2000 and 2003, fueled by the dot com collapse and 9/11.

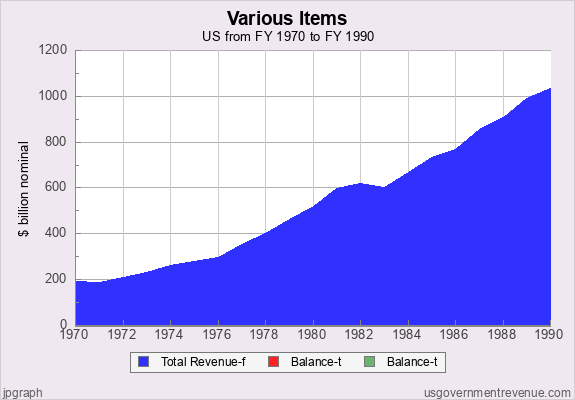

Its simple to understand that evenue rises as GDP goes up, as population rises and more people enter the workforce, and as people live and work longer. This explains Graham's disingenuous statistical analysis through which he attempts to show that revenue has continually risen over decades while through both high and low tax periods:

Note that Graham has just provided, unwittingly perhaps, the very evidence against his own argument that Laffer and other free market economists would point to as evidence of their claims. Look at the graph. At the end of the Nixon and Carter years (both liberal, interventionist Keynesians given to high taxes, deep government regulation, and price controlling), government revenue was well under half of what it was after the seven year supply side boom of the eighties.

Again, Graham has two fundamental problems here, the first being that he simply does not understand basic free market economics, and the second being his disdain and rejection the disciplines of critical thinking in his quest for a quick ideological/psychological fix.

Tax revenues are not correlated with tax rates but with economic growth. That's the fundamental theoretical and historical principle involved. This is why leftists like Graham, who's primary purpose is not to understand economics but to offer sacrifices to their god, government, continue to make illogical and counter-intuitive claims that rising tax burdens, and even substantial ones, increase government revenue.

That's simply a plea for the static, interested political class/statist position that Laffer has termed the "arithmetical". What actually occurs, however, is an

economic effect, a "catallactic" effect based upon rational human being's perception of and reaction to economic incentives and environments. Increasing tax rates would increase government revenue - in an econometric mathematical model or in a formal deductive argument. In the real world, however, devoid of the need for ideological purity and emotional venting at personal mythological enemies, human behavior changes; economic activity recedes, the tax base shrinks, and government revenues wilt.

Note also in Graham's graph the big dip just at the 1982 to 1983 mark; that's the second major Carter-Keynesian recession coming out of the 70s, while the economy was hemorrhaging jobs and capital and the Reagan tax cuts were in their phase in stage. Then notice in 1984, when the tax cuts become fully active, the economy does what? Yes, it takes off, and takes off dramatically. By 1990, government revenue comes in at just over a trillion dollars, as compared to the roughly $500 billion that ended the economically disastrous Carter years, which themselves were simply more dramatic extensions of Nixon's policies.

If I give Kevin enough rope...well, you know.

Now, let's discuss Kevin's quaint Michael Mooresque leftist class war fables about the Bush tax cuts. What is the truth here?

Well, in the first place, let's revisit the claim that the Bush tax cuts reduced revenue and increased the deficit. Kevin can use his carefully selected graphs to show correlations between the Bush tax cuts and revenue decreases. Did they decrease? Yes, they did, as the cuts were being phased in over several years. Were the cuts the cause of the revenue decreases. In the interim, perhaps (and there is nothing wrong with deceased government revenues, by the way), but tax revenues in 2006 were actually higher than the projected levels that existed before the 2003 cuts ($47 billion above the projection)

What were the projections for revenue? Well, the CBO had predicted that the 2003 cuts would lower revenue by some $75 billion (and this is the product of the long discredited - but politically useful "static" scoring method used by such government agencies, which makes no attempt to capture actual changes in economic behavior generated by government policy). What actually happened? 2006 revenues were $47 billion above the pre-tax cut assumptions.

The Bush cuts appear to have actually recovered lost revenue and stimulated the economy (not self negating, debt creating and wealth destroying Keynesian "stimulus" , but the actual stimulating of private sector wealth creation through the stimulation of risk, investment and entrepreneurship - work).

Were the Bush tax cuts good for the economy, or a detriment? As usual, Red Kevin Graham is wrong yet again:

What taxes were lowered in the Bush cuts? Income, dividend, and capital gains taxes. In other words, these tax cuts were aimed primarily at the job and opportunity creating elements of society, the purpose of which was to incentivize work, savings, investment, and risk - wealth creation. What happened? Look at the empirical evidence above.

Wherever you look, Kevin's claims appear to be on life support. Non-residential fixed investment was in decline for 13 consecutive quarters before the Bush cuts. What the happened after their full phasing in? Thirteen consecutive quarters of expansion is what happened, along with a boom in the S&P and increases in dividend payments.

But please don't get the idea that because of the primary targets of the tax cuts, this was a "tax cut for the wealthy" the poor, hoary, wheelchair-bound class warfare shibboleth of the Ruling Class that has kept so many demagogues in power for so long at the expense of so many.

Actually, following a dramatic trend that began under Reagan, the rich are now paying the vast majority of all income taxes paid, as they paid in ever rising percentages from Reagan through the present time. Did the millionaire save more for a 1% cut in taxes than the guy making $25,000 a year? Of course, because those low income household pay almost nothing in income taxes, while the millionaire paid much more into the system to begin with.

Despite Graham's populist class warfare mythology, the Bush tax cuts shifted even more of the tax burden toward the wealthy, following a a consistent trend over several decades. good heavens, by the year 2000, the top 60% of American taxpayers were shouldering virtually 100% of all income taxes paid. Meanwhile the bottom 40% paid no income taxes at all. How then, one might want to ask economics expert and moral philosopher Kevin Graham, could politicians give takes breaks to people who...pay no taxes.

Well, Obama has done just that (the now infamous Obama "tax cuts" that are actually tax "credits" that will actually provide "tax cuts" (government checks) to some 44 million Americans who pay no income tax at all), but giving a tax cut to those who pay no taxes is not a tax cut, but a welfare payment - a government income transfer, not a tax cut.

This is actually a very disturbing development for a constitutional republic and a free society, as a society in which the vast majority pay no income taxes, but receive government largess and gratuities from the revenue of the tiny percentage who do, is a society that is creating a vast body of lower classes dependent upon government for much of their lot in life, funded my a tiny, productive minority of job creators.

As the ravenous appetite for more government "benefits" grows, and as the ability of the economy to sustain those benefits shrinks, the mentality of class warfare will move from smoldering ember to raging brush fire, and we will be living in a society in which a clear majority of citizens are dependent upon government for much of their position and security in life. A massive, perhaps overwhelming constituency that supports leviathan government, the nanny state, and an entrenched political class and which lives parasitically on the wealth created by the job and opportunity creating minority will have been created that has no further interest in the limited government, individual liberty, or the rule of law.

That will be the end of the republic as we know it and as the Founders created it.